Overview

We tried to predict where Bitcoin's price would go next using only its own price history.

- Bitcoin is a volatile, decentralized cryptocurrency whose price has risen and fluctuated dramatically since 2017.

- Goal: forecast monthly Bitcoin closing prices using only the historical price series itself.

- Approach: classical univariate time-series modeling (AR, MA, ARMA, ARIMA).

- Hold out the last 12 months as a test set to honestly measure out-of-sample forecast accuracy.

- Challenge acknowledged up front: extreme volatility limits how far a price-only model can see.

Methodology

flowchart LR A[Raw Data] --> B[Clean & Encode] B --> C[EDA] C --> D[Train/Test Split] D --> E["Models"] E --> F["Tune (Cross-Validation)"] F --> G["Evaluate: R2 / RMSE"]

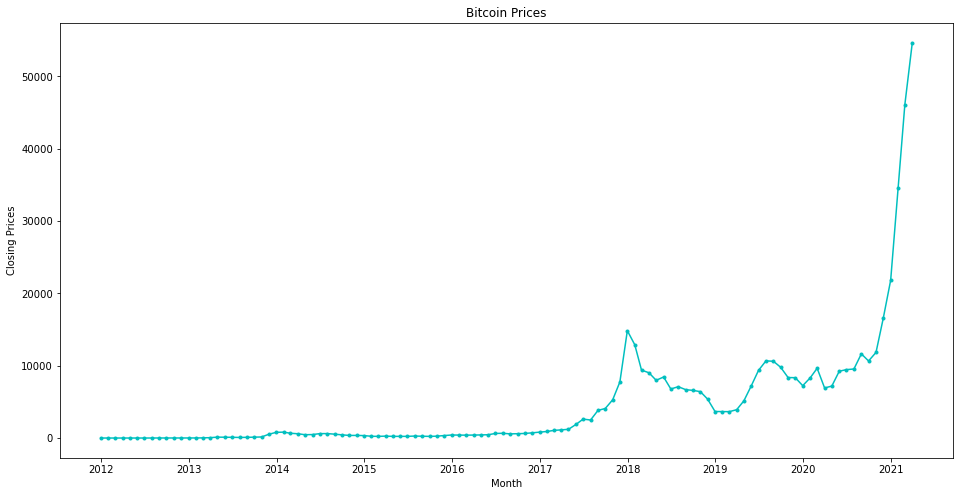

The Data

We worked with about nine years of monthly Bitcoin closing prices, with no gaps in the record.

- Dataset has 112 monthly observations across 2 columns: Timestamp and closing price.

- Timestamp was object-typed and converted to datetime, then set as the series index.

- Closing price stored as float; no missing values anywhere in the dataset.

- Split: final 12 months held out as test data, the rest used for training.

- Prices show a strong upward trend with rapid fluctuations, especially during 2021.

Exploratory Analysis

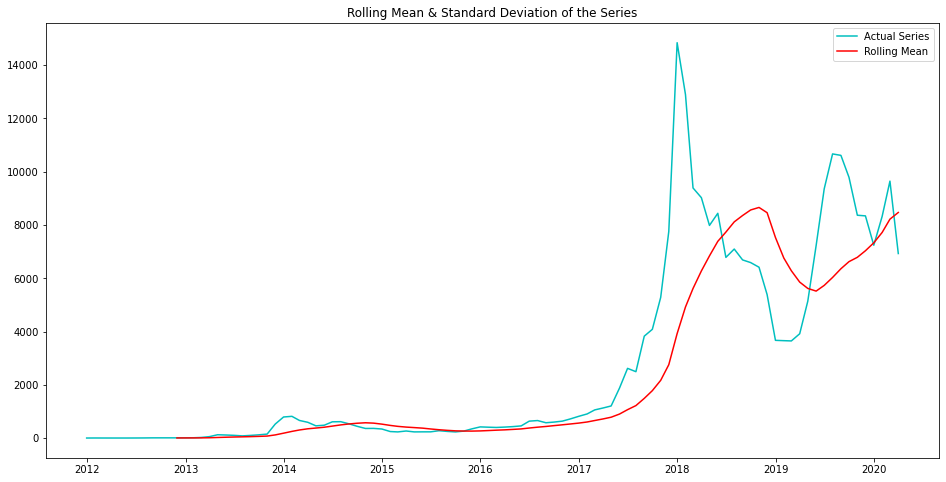

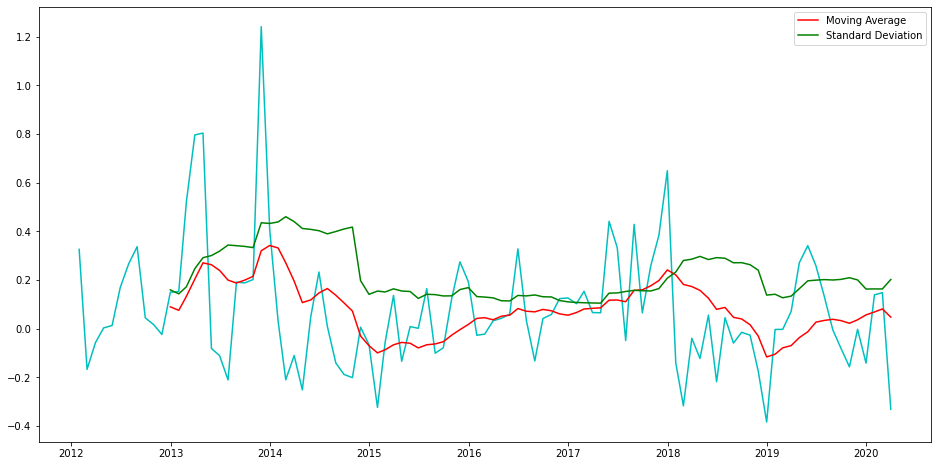

We checked whether the price pattern was stable over time, and it clearly was not.

- Rolling mean and standard deviation revealed a clear upward trend, signaling a non-stationary series.

- Augmented Dickey-Fuller test gave a p-value of about 0.36, far above 0.05.

- We failed to reject the null hypothesis, confirming the raw series is non-stationary.

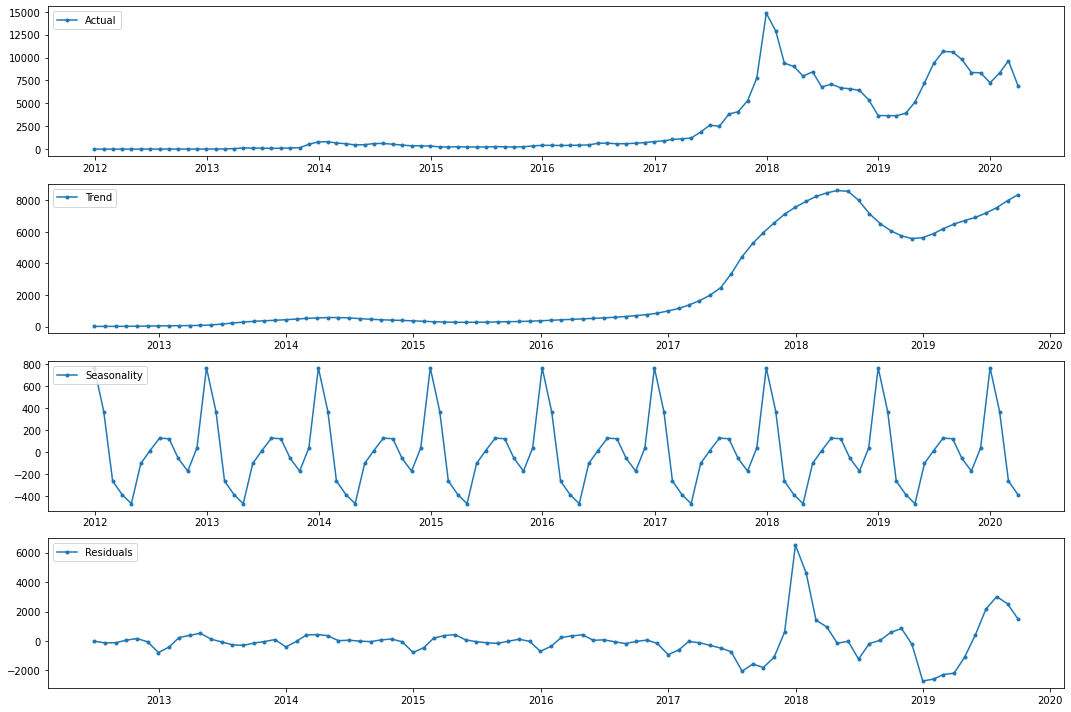

- Decomposition exposed distinct trend, seasonality, and residual components.

- Seasonality showed prices spiking from December to January, then declining steadily through May.

Time-Series Patterns

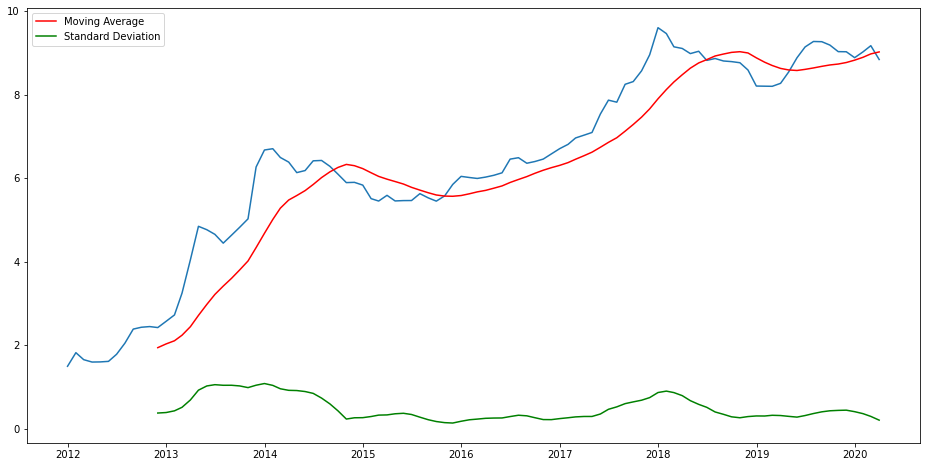

We transformed the data until the price pattern became stable enough to model.

- Log transformation stabilized variance but left the upward trend intact, so still non-stationary.

- Differencing by lag 1 (one month) produced a constant mean and standard deviation.

- Post-differencing ADF p-value fell well below 0.05, confirming the series was now stationary.

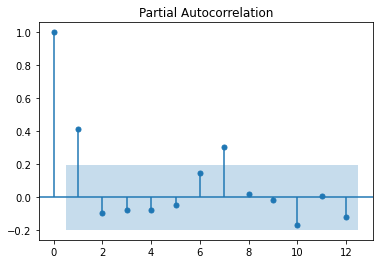

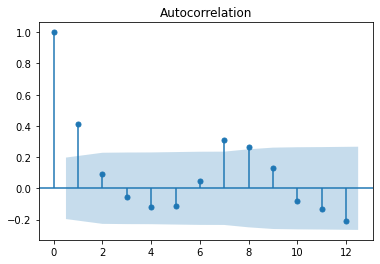

- PACF plot's last significant lag was 7, suggesting an AR order of p = 7.

- ACF plot similarly indicated q = 7, setting the orders for the ARMA and ARIMA models.

Modeling & Results

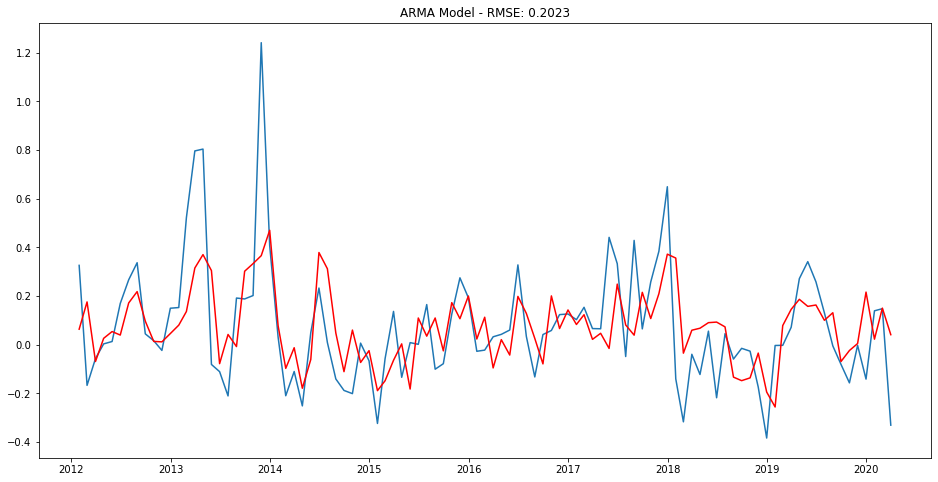

We compared four forecasting models and the ARMA model gave the most accurate predictions.

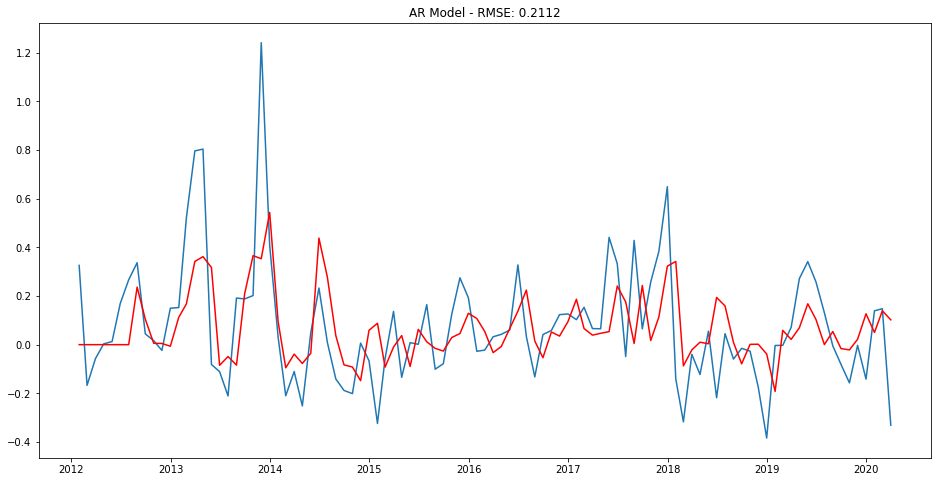

- AR model (p=7) achieved an RMSE of 0.2112 on the log-differenced series.

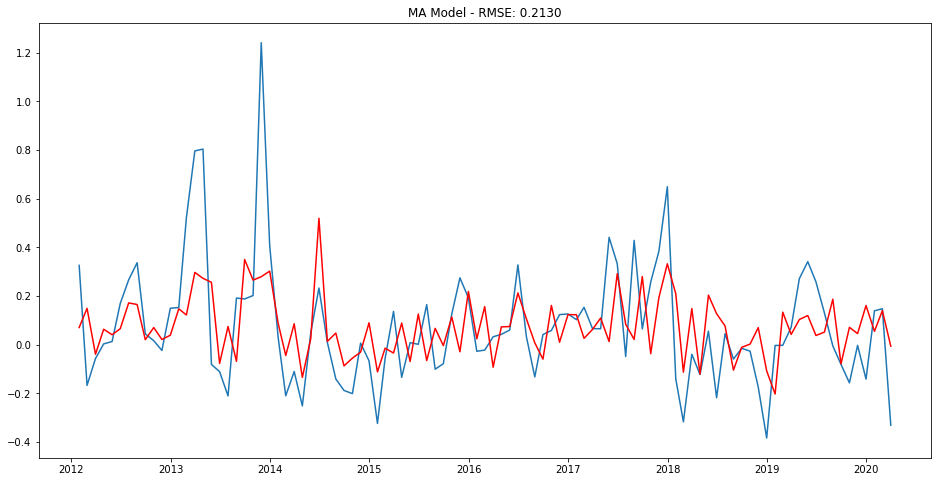

- MA model scored a slightly higher RMSE than AR but a lower AIC, fitting the training data better.

- ARMA model (p=7, q=7) delivered the lowest RMSE of all four models.

- ARIMA model (p=7, d=1, q=7) gave the highest RMSE and much higher AIC, so it was dropped.

- ARMA chosen as the final model: best RMSE and second-lowest AIC overall.

Key Takeaways

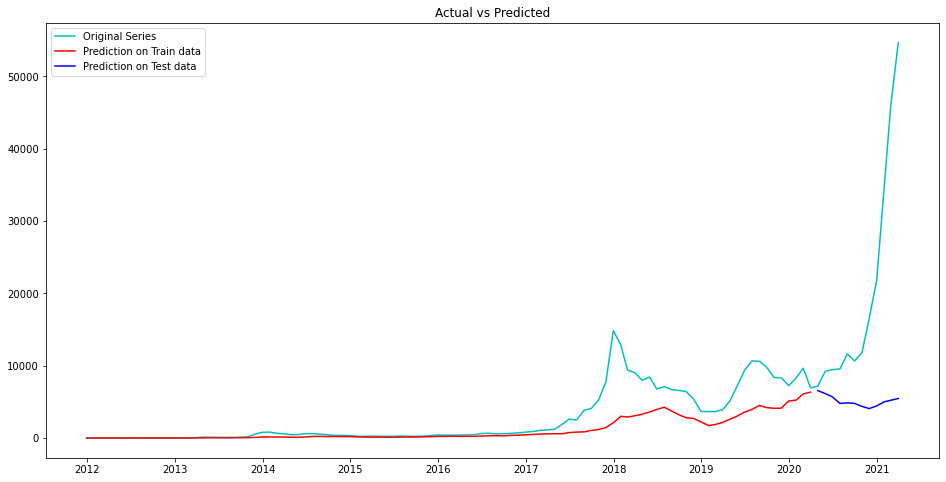

The model fit history well but struggled to forecast the future, which is expected for such a volatile asset.

- Training-data predictions tracked actual prices closely, except for spikes in 2018 and late 2019.

- On the 12-month test set the forecast drifted far from actuals, with RMSE much higher than training.

- The gap reflects Bitcoin's extreme volatility and external drivers a price-only model cannot capture.

- Honest conclusion: classical models capture trend and seasonality but cannot reliably predict crypto prices.

- Built with: pandas, numpy, matplotlib, statsmodels 0.12.1

More Visualizations

Tech Stack

- pandas — data wrangling and tabular manipulation

- numpy — fast numerical arrays

- scikit-learn — modeling, pipelines, and evaluation

- seaborn — statistical visualization

- matplotlib — plotting

- statsmodels — OLS / statistical inference & VIF

Attribution

This project was completed as part of the MIT Applied Data Science Program (MIT IDSS / Great Learning). The program provided the case-study scaffolding; the analysis, code, and results are my own. Published with permission, for portfolio use only.